N26 Review

N26 Bank AG · Berlin · BaFin-regulated

N26 has been the default first account for expats arriving in Germany for nearly a decade. The fully English app, eight-minute opening process, and willingness to onboard newcomers without Anmeldung or an established Schufa record still set it apart from every traditional bank. This review covers what has changed in 2026, what the free plan actually includes, and where N26 falls short compared to newer competitors.

Still the best day-one account for expats arriving in Germany. The free Standard plan is more limited than before, but unbeatable for getting a German IBAN in under ten minutes.

N26 website and app interface, June 2026

What is N26?

N26 is a fully licensed German bank (N26 Bank AG), headquartered in Berlin and regulated by BaFin, the Federal Financial Supervisory Authority. Founded in 2013, it grew into one of Europe's largest neobanks and serves over 8 million customers across Europe. Unlike e-money apps, N26 holds a full German banking licence, which means your deposits are protected up to 100.000 € under the German statutory deposit guarantee scheme.

For expats in Germany, N26's defining advantage has always been its entirely English-language experience. The app, the website, all legally binding contracts, and the customer support chat operate in English. In a country where less than 5 % of traditional banks offer an English-language interface, this alone makes N26 the default starting point for international residents.

N26 website and app interface, June 2026

N26 does access Schufa data when you apply, but a blank record (no history at all) does not prevent account opening. This is the situation of almost every newcomer. A low or non-existent score is treated differently from active negative entries. In practice, N26 accepts the vast majority of new arrivals without issue.

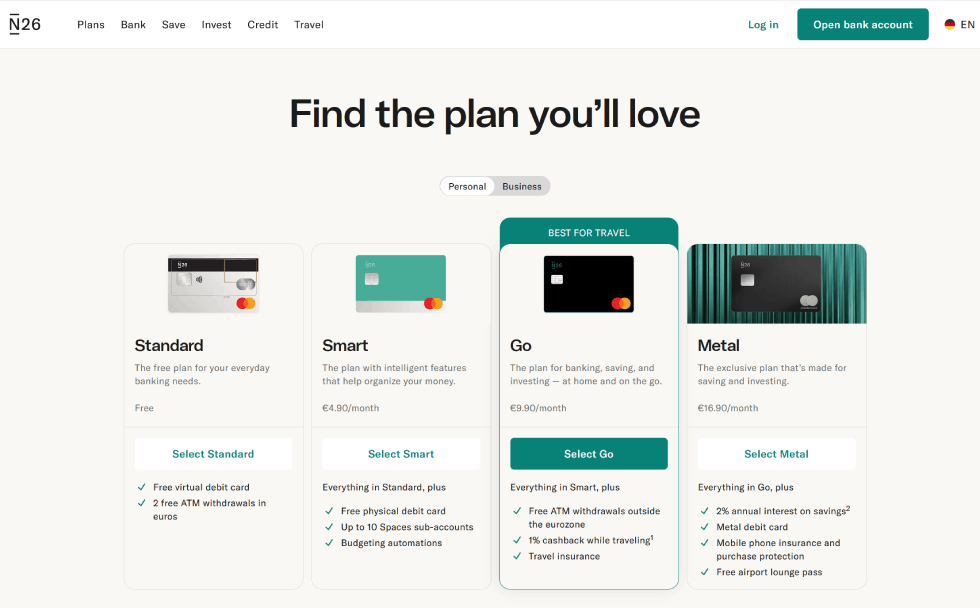

N26 account plans compared

N26 offers four account tiers in 2026. For most expats, the choice is between Standard (free) for the first months and Go or Metal once they travel frequently. Smart sits in an awkward middle position.

N26 Standard

- German DE IBAN, free forever

- Virtual Mastercard included

- 3 free ATM withdrawals/month (in Germany)

- Free card payments worldwide

- SEPA instant transfers, Apple/Google Pay

- Fee-free trading: stocks and ETFs in-app

- Physical card: one-time 10 € delivery fee

- 1,7 % fee on ATM withdrawals outside Eurozone

- No Spaces sub-accounts

- No phone support (chat only)

N26 Smart

- All Standard features

- Up to 10 Spaces sub-accounts with own IBAN

- 5 card colour options

- Shared Spaces with partner

- Physical card delivery included

- Still 1,7 % on non-Euro ATM withdrawals

- No travel insurance

N26 Go

- All Smart features

- Unlimited free ATM withdrawals worldwide

- No foreign currency fee outside Eurozone

- Comprehensive travel insurance (Allianz)

- Phone support included

- eSIM data plans in-app

N26 Metal

- All Go features

- Metal stainless steel card

- Extended travel insurance coverage

- Crypto fee discounts

- Priority customer support

- Airport lounge access (purchasable in-app)

N26 fees explained

The Standard plan is free, but specific actions carry costs that catch many newcomers by surprise. This table covers every fee that commonly applies to expat usage.

| Fee type | Standard | Smart | Go | Metal |

|---|---|---|---|---|

| Monthly fee | 0 € | 4,90 € | 9,90 € | 16,90 € |

| Physical card delivery | 10 € (one-time) | Included | Included | Included |

| Card payments worldwide | Free (unlimited) | Free | Free | Free |

| ATM withdrawals (€, Germany) | 3 free, then 2 € each | 5 free, then 2 € | Unlimited free | Unlimited free |

| ATM withdrawals (outside Eurozone) | 1,7 % fee | 1,7 % fee | Free | Free |

| Foreign currency fee (card payments) | 0 % | 0 % | 0 % | 0 % |

| SEPA transfers (outgoing) | Free | Free | Free | Free |

| Cash deposits via CASH26 | 1,5 % (above 100 €/month) | 1,5 % | 1,5 % | 1,5 % |

| Overdraft (Dispo) interest | 13,4 % p.a. | 13,4 % | 13,4 % | 13,4 % |

| Travel insurance | No | No | Yes (Allianz) | Extended |

N26 Standard no longer includes a free physical card. A one-time 10 € delivery fee applies when you order the Mastercard. The virtual card for Apple Pay and Google Pay is always free and available instantly after account opening. If you want a physical card from day one, order it during the application process.

App features and daily banking

The N26 app is consistently rated among the best-designed banking apps in Europe. Every core function works smoothly, real-time push notifications arrive within seconds of a transaction, and the interface requires no German knowledge at any point.

What works well

-

Instant transaction notificationsReal-time push alerts for every payment, in English

-

Card controlsLock and unlock your card instantly in the app. Restrict online payments or ATM withdrawals independently.

-

Spending statisticsAutomatic categorisation of all transactions. Monthly spending breakdown by category.

-

In-app stocks and ETF tradingFee-free stock and ETF trading directly from the N26 app. Available on all plans.

-

N26 for under-18sParents can open a linked debit card for children aged 7 to 17 with adjustable spending limits. Useful for families relocating to Germany.

Known limitations

-

No GirocardThe single biggest practical gap. Shops displaying "Nur EC" or "Kein Visa" will not accept N26. Carry cash or add a C24 account for Girocard acceptance.

-

No physical branchesAll support runs through the app chat or phone. Complex issues (disputes, fraud) can take days to resolve through chat alone.

-

Phone support: paid plans onlyStandard and Smart users can only contact support via in-app chat. Wait times can be long during peak periods.

-

Cash deposits are costlyCash deposits via CASH26 at Rewe or Penny are free up to 100 € per month, then 1,5 %. Not a good fit for anyone who regularly handles cash income.

-

Nationality restrictionsN26 does not accept all nationalities. Check the accepted ID list at n26.com before applying.

Category ratings

Bankdaten.de rates N26 across seven criteria relevant to expats and newcomers in Germany.

App, website, contracts, and support: entirely in English. No competitor matches this.

8 minutes, no Anmeldung, IBAN immediately. Nothing faster exists in Germany.

Among the best-designed banking apps in Europe. Instant notifications, clear categorisation.

10 € card delivery fee and only 3 free ATM withdrawals/month have weakened the free tier. C24 Smart is now a stronger free account for settled residents.

No Girocard is a real-world limitation in Germany's cash and EC-Karte culture. Mastercard works in most places, but not all.

Chat support is in English but response times vary. Phone support is restricted to Go and Metal. Complex issues can take several days to resolve.

Full German banking licence, BaFin-regulated, statutory deposit protection up to 100.000 €.

N26 is a good fit if…

Good fit for you

Consider alternatives if…

The most practical setup for most expats is N26 Standard on day one (English, no Anmeldung), then C24 Smart after Anmeldung (free Girocard, interest on balance). Both accounts are free. Together they cover every payment scenario in Germany and abroad.

Frequently asked questions

Ringo Dühmke, Bankdaten.de

N26 Standard remains the best day-one account for expats arriving in Germany. Nothing else delivers a German IBAN in eight minutes in full English with no Anmeldung required. The free plan is leaner than it used to be, but for the first six to twelve months in Germany it does exactly what you need. Once settled, add C24 for the Girocard and interest on your balance, and consider upgrading to N26 Go if you travel regularly outside the Eurozone. The two-account combination costs nothing and covers every payment scenario in Germany.